3.1 Potential Alternative Methods

In this section, we explore feasible methods to estimate cash yields for private companies and also highlight their limitations on why they cannot be used in our application.

Actual dividend data

When actual dividend data along with the payout dates are extensively available for private companies, then dividend adjustments in index computations are fairly straightforward and can be done in a manner as other popular publicly traded indices such as MSCI Total Return Indices (MSCI Inc., 2012) or the Dow Jones Industrial Average Total Return Indices (S&P Dow Jones Indices, 2023). Typical adjustments for equity indices assume that the amount of dividends generated in the same currency as the index (converted if dividends are paid in a different currency) on the ex-dividend date are reinvested in the index to compute total returns. Thus, if the amounts and dates of dividends of private companies are known, similar computations can be performed.

However, a problem with such an approach is the lack of dividend data for private companies. Even vendors who are expanding their coverage of private company data deprioritise collecting their dividend information. Unless required by regulations (e.g., specific countries), private companies seldom have the incentive to report their dividends to third-party vendors, thus creating a dearth of dividend data. This complicates building a cash yield model for private companies.

For example, from a vendor specialising in private company-level data, we observed a sample of 12,538 companies, and only 2.16% of the companies were observed to pay dividends. Also, among the non-dividend payers, it is not possible to interpret them as not paying dividends or dividend information is missing. Such sparse coverage makes it difficult to put together any large sample of actual dividend data.

Table: Vendor data on dividend payout ratios of private companies | ||

Payout ratio (in popular vendor) | Number of observations | % of sample |

Non-zero values | 271 | 2.2% |

Zeros | 11,185 | 89.2% |

Missing | 1,082 | 8.6% |

We also repeat the procedure with another alternative vendor providing private company financials and find the coverage of non-zero dividend information to be even poorer (less than 0.2% of tracked companies).

Does this lack of dividend data arise from private companies not paying dividends or vendors not capturing it? Although we believe it is the latter, some checks confirm that vendors fail to capture dividend information. Using financial statements of private companies that are publicly available, we check a private company in each of these databases.

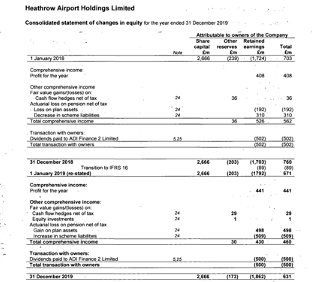

Heathrow Airport Holdings Financial Statements (original resolution and quality)

As seen above in this poor resolution direct filing of a UK-based private company, Heathrow Airport Holdings does disclose dividends paid in 2019 to its corporate parent, the same entity captured by both the vendors we consider. However, neither of them captures the dividend paid and assumes 100% of earnings are retained.

Thus, using direct data from either the private company, which is reported to regulators, or those obtained through vendors are not feasible options as they present an unrealistically low estimate of dividends.

Estimate dividends through indirect methods

When actual dividend data is not available, it may be possible to compute dividends from detailed financial statements observed over successive financial periods. For example, dividends can be inferred as the difference between retained earnings in successive financial years and net income generated during the financial year. For example, if the balance sheet indicates retained earnings of a private company as $2.1 million in 2021 and $2.3 million in 2022, while the comprehensive income during 2022 was $250 thousand, then dividends paid out must be $50,000 during 2022.

Although, in theory, these calculations may work, they require that we have both retained earnings, net income, or comprehensive income available for different financial periods. Exploring vendor data, even for notable private companies, such data is not available.

Thus, this method is also not feasible to estimate the dividends of private companies.

Model using public markets data

Private companies are similar to publicly listed ones in many ways, including facing similar market opportunities and threats, operating in similar industrial activities, attracting institutional interest for shareholding, having similar capital structures, and being exposed to similar business cycle fluctuations. Thus, building a dividend model using purely public market data is an option.

However, Michaely and Roberts (2006) study the dividend policies of private companies and find significant differences between dividend policies in public and private ones, including:

No evidence of dividend smoothing in private companies, whereas public companies follow smoothened dividend policies characterised by slowly increasing dividends and infrequent decreases.

Dividend policies of private companies are erratic and more sensitive to transitory earning shocks, indicating that payouts are a residual financing decision.

Also, public companies distribute a larger fraction of earnings as dividends, and these dividends are more sensitive to investment opportunities.

These differences indicate that public companies and their dividends will be poor inputs to model the payout policies of private companies if used as the only inputs.

Michaely, R., & Roberts, M. R. (2006). Dividend Smoothing, Agency Costs, and Information Asymmetry: Lessons from the Dividend Policies of Private Firms. Duke University. https://faculty.fuqua.duke.edu/corpfinance/papers/2006.MichaelyRoberts.pdf

MSCI Inc. (2012). MSCI Index Calculation Methodology. MSCI. https://www.msci.com/eqb/methodology/meth_docs/MSCI_May12_IndexCalcMethodology.pdf

S&P Dow Jones Indices. (2023). S&P Equity Indices Policies & Practices. S&P Dow Jones Indices. https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-equity-indices-policies-practices.pdf