1.2 Data Types

Infrastructure is a relatively new asset class, and official guidance by standard-setting institutions on what information is required to assess performance in a consistent and meaningful manner is lacking.

Scientific Infra & Private Assets has developed a global data standard to guide investors and contributors regarding what data types are necessary for inclusion in the Scientific Infra & Private Assets indices.

In this section, we describe the type of data that may be observed, collected, and reported for each firm, and we briefly discuss how it may be structured, drawing a fundamental distinction between static and dynamic data. We do not discuss what relevant proxy or market data can also be collected for the purpose of asset pricing. These points are discussed from the point of view of IFRS 13 and modern asset-pricing theory in the Unlisted Infrastructure Asset-Pricing Methodology.

Observable Data Types and Attributes

Each investment in private infrastructure debt or equity relates to an individual firm – often a project-specific firm – hence the individual firm is the relevant level of observation.

A first step consists in the identification of a unique investable infrastructure company, and whether it is considered an equity investment or a borrower. Firms have a name and a location (of their tangible assets), a registration number, and other fixed characteristics that make them uniquely identifiable[1]. For each identified firm, two types of observable data points are of interest:

Cash flows (and cash flow ratios). Next, the cash flow and event data need to be categorised according to economically meaningful attributes. These fall into two main categories:

Physical attributes of the firm: what and where the firm is as an infrastructure investment; and

Business-model attributes of the firm: sources of revenues and costs of the firm and whether or not the risk inherent in these exposures is insured against (transferred) via contracts with third parties.

Finally, the investable character of each firm is represented by a set of financial instruments found on the firm’s balance sheet (on the liability side). These instruments also have their own attributes: type of payout structure, control rights and terms applicable to the different claimants to the firm’s free cash flow.

The figure below provides a summarised illustration: the firm’s "event" and "cash flow" data, as well as its attributes and those of its instruments, can be collected at different points in time and may also change each time they are collected.

Data Types and Attributes of Private Infrastructure Investments

Dynamically Reported Data

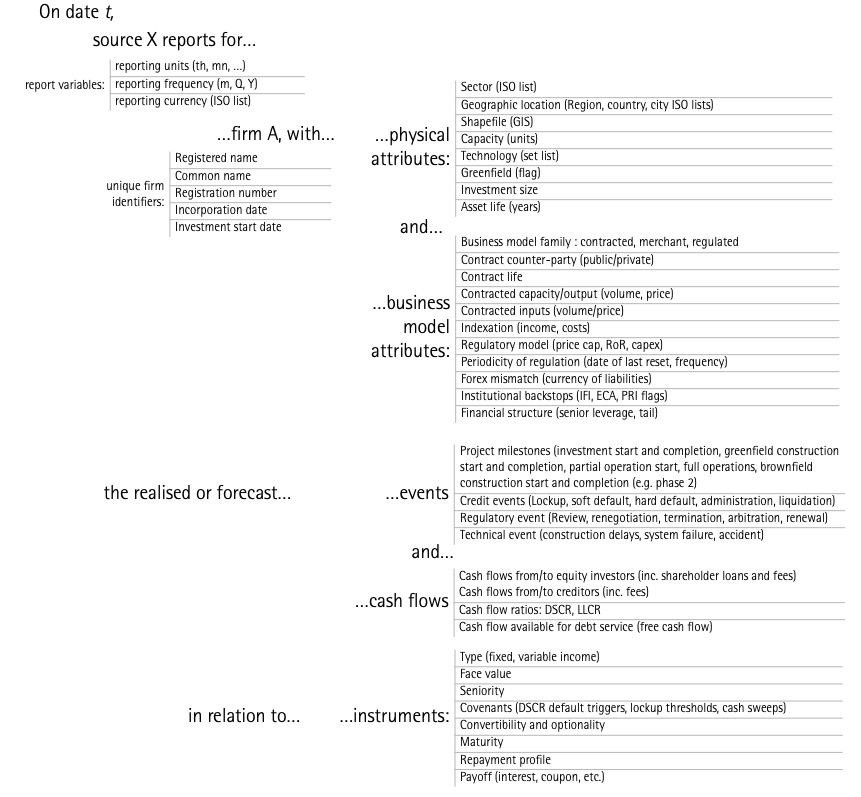

As proposed above, all relevant observations must be reported at the firm level. For each firm, individual observations can be captured in a report, as illustrated in the figure below.

Reporting Data and Attributes of Private Infrastructure Investments

Reports simply reflect the fact that some information about an investable infrastructure company is reported at some point in time, by a given source, and includes data on events or cash flows, or the physical and business-model attributes of the firm, or indeed any of the relevant financial instruments and what their attributes are at that point in time.

At the time of the report, this information can either be realised or predicted. Hence, to ensure consistency between sources and time frames, each reported data point must be placed on a double time scale:

the time of reporting; and

the reported time of occurrence (which can be in the past, present, or future relative to the time of reporting).

For example, the latest annual accounts report today which cash flows and events occurred last year; likewise, the financial-close cash flow model reports which cash flows and events are predicted to occur over the next 25 years, at that point in time. In other words, all firm and instrument attributes should be reported and recorded dynamically. For instance, a loan may change interest rate over time (and this may be known in advance), or a firm may see its take-or-pay off-take contract expire before the end of the investment’s life. If this contract-expiry date is also known in advance, a future contract expiration event can be reported, until the event occurs, at which point it becomes a realised observation.

Capturing realised and forecast changes in time of the attributes of either firms or instruments is of particular importance in the case of infrastructure investments because of the path-dependency and sequential resolution of uncertainty, which characterises these types of investments. For example project debt may change its maturity date post-restructuring, which is instrumental in the context of asset pricing and computing duration. Importantly, because of the long-term nature and large sunk costs implied by such investments, long-range cash flow projections and detailed financial models are well documented and frequently revised. All such data points are therefore observable.

The rest of the data collection process flows from the sequencing of individual reports, which are cross-referenced across sources of information, for each identified investable infrastructure firm. Individual reports can correspond to a single data point, realised or forecast, at one point in time, or to the entire set of accounts of the firm in a given year, or to the base case cash flows corresponding to a single instrument for the next two decades.

This framework is flexible enough for all such types of observations.

As the figure above illustrates, each report is made in a given unit, currency and for a given periodicity of the data, allowing future manipulation of any contributed data while ensuring consistency and comparability. Reports are also source-specific. Firms are thus uniquely identified and by cross-referencing source-specific reports manually or using algorithms.

[1] While this information is not always fully available (e.g., certain data contributors are required by law to anonymise any contributed data), it can also be recouped from multiple sources. It is important to ensure that individual observations are not double-counted or duplicated; hence, arriving at unique identifiers for the firm data being collected matters significantly.