Choice of factors for unlisted infrastructure equity

The following systematic five key risk factors are used by infraMetrics® to estimate a model of the expected returns using observable market prices as inputs, as well as several control (dummy) variables that account for sector and business model specific effects.

Factor Name | Factor Definition | Factor Interpretation |

|---|---|---|

Size | Total Assets | Larger infrastructure companies are more illiquid and complex than relatively smaller ones. The size factor systematically attracts a positive premia. |

Profit | Return on Assets before Tax | More profitable firms are more valuable. Higher profits thus tend to attract a lower premia. The factor premia or |

Investment | Capex over Total Assets | During the development or greenfield phase of infrastructure companies, relatively large capital costs are incurred and sunk. This is a riskier period, and a higher ratio of capital expenditure to size attracts a higher expected return, i.e. a positive risk premia. |

Leverage | Total Liabilities over Total Assets | Likewise, controlling for other effects, higher leverage signals higher risk and is characterised by a positive risk premia. |

Term | 20-year public bond yield minus 3-month public bond yield | The slope of the yield curve can be a good proxy of country risk, both political and macro-economic. The term spread is computed as the time of each valuation, using the relevant curve in the country of the investment. A higher term spread is characterised by a positive risk premia and thus a higher aggregate risk premia. |

TICCS® Business Risk | Merchant, Regulated or Contracted control variables | Controlling for business risk families as defined in TICCS® shows that merchant companies systematically attract a higher risk premia, i.e. expected returns are higher in riskier segments of the infrastructure market. |

TICCS® Sector | Industrial activity superclass or class control variables | Likewise, a few sectors are found to have systematically higher or lower expected returns even after controlling for the effect of the factors described above, e.g. renewable energy projects have systematically lower returns (or higher prices) even for similar size, profits, leverage etc. |

' aria-hidden='true'%3e %3cuse xlink:href='%23E1-STIXWEBNORMALI-1D706' x='156' y='-50'%3e%3c/use%3e %3c/g%3e %3c/svg%3e) is negative. As a result, during the greenfield phase, when profits are also negative, or in periods of distress, this factor carries a positive premia.

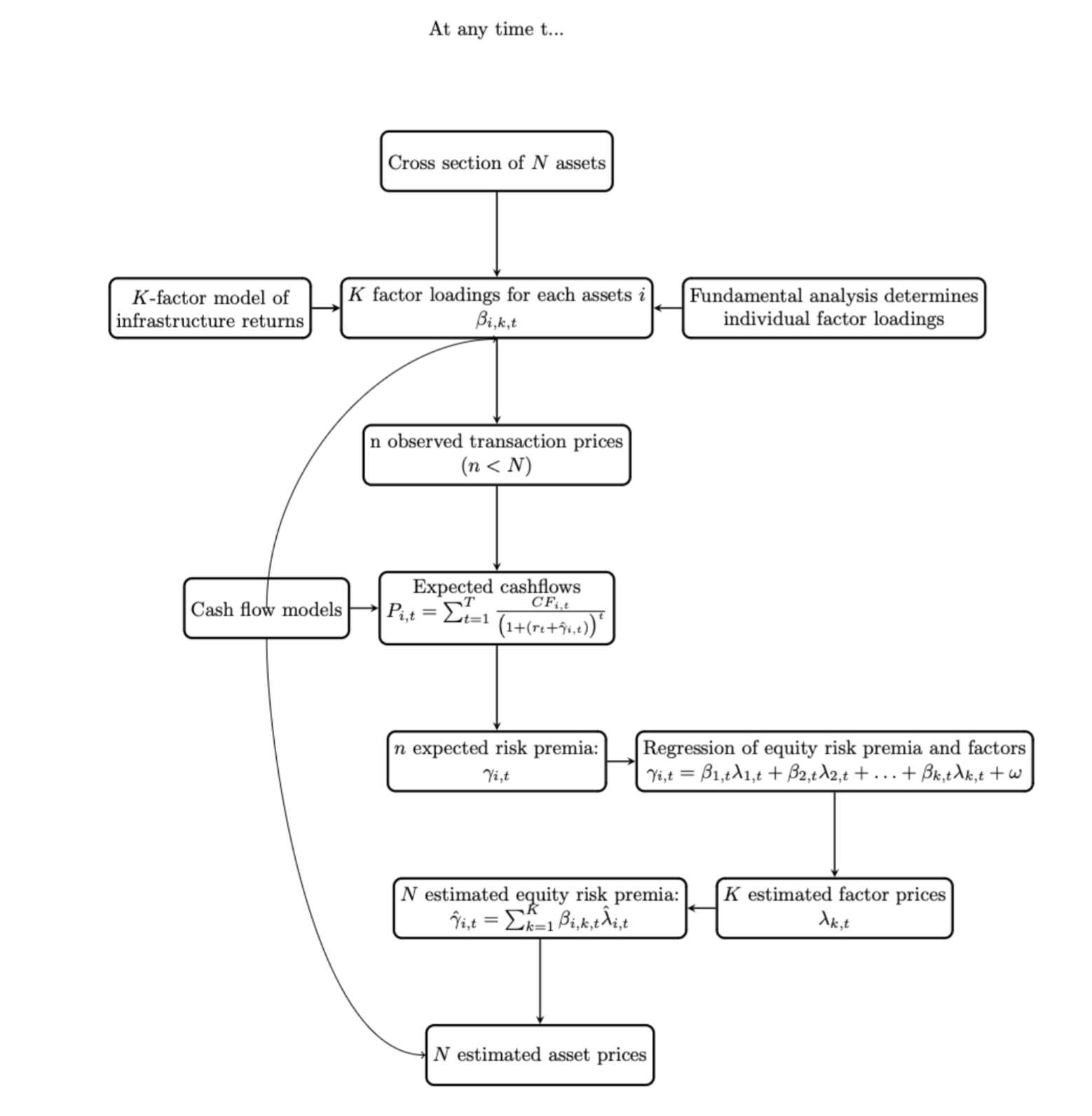

is negative. As a result, during the greenfield phase, when profits are also negative, or in periods of distress, this factor carries a positive premia. Summarising diagram for the estimation of risk factor premia for unlisted infrastructure assets