1.4.1 Interest rate curves

The Scientific Infra & Private Assets approach to computing the value of unlisted infrastructure companies' equity (or debt) requires using a term structure of interest rates at the time of valuation and to the relevant investment horizon. Interest rate curves (or term structures) are needed both when extracting observed risk premia from secondary market transactions and later when computing asset values.

All asset values are computed using a discounted cash flow (DCF) approach, requiring an estimate of the 'risk-free' rate of interest along with the infrastructure equity risk premia at the time of valuation. This last point plays an important role in the achievement of fair market value estimates. IFRS 13 guidance requires using the most relevant market inputs at the time of the asset valuation.

Example

When observing a deal IRR or pricing the equity of a wind power generation company with a 20-year life in Spain in the 3rd quarter of 2012, a 20-year term structure of the Spanish government bond yields in that quarter is needed and estimated.

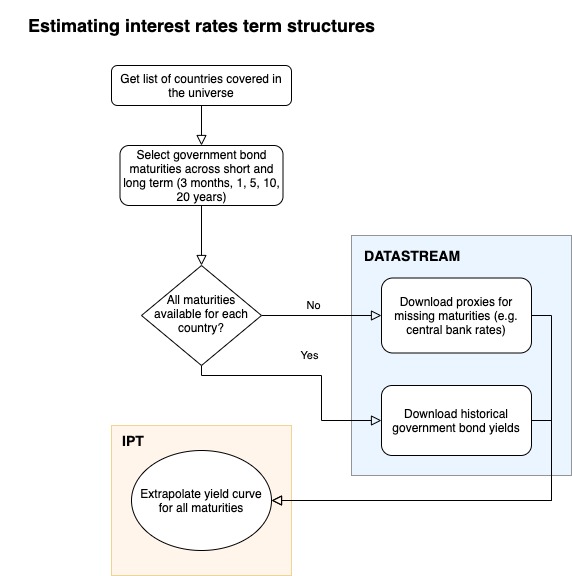

To this end, government bond yield curves are computed for each valuation date (Month end date) since 2000 for all horizons up to 100 years. This is done for each country included in the Index Universe by interpolating observable market rates as described below.

Raw data

Raw interest rate data is sourced from DataStream® using the following rules:

Government bond yield benchmark for short (

' aria-hidden='true'%3e %3cuse xlink:href='%23E1-MJMAIN-2264' x='156' y='-50'%3e%3c/use%3e %3c/g%3e %3c/svg%3e) 24 months), medium (> 24 months 7-year) and long-term maturities (> 7 years).

24 months), medium (> 24 months 7-year) and long-term maturities (> 7 years).ON (overnight) or TN (tomorrow next) rates, for yields below 1 year maturity.

Input data that does not change more than three consecutive quarters is dropped to avoid stale inputs.

Model

The yield curve is given by the following function (Nelson-Siegel-Svensson or NSS model):

=b_0 %2b b_1 %5cfrac%7b1-e%5e%7b-m/%5clambda_1%7d%7d%7bm/%5clambda_1%7d%2bb_2(%5cfrac%7b1-e%5e%7bm/%5clambda_1%7d%7d%7bm/%5clambda_1%7d-e%5e%7b-m/%5clambda_1%7d)%2bb_3(%5cfrac%7b1-e%5e%7bm/%5clambda_2%7d%7d%7bm/%5clambda_2%7d-e%5e%7b-m/%5clambda_2%7d)%5cend%7barray%7d%3c/title%3e %3cdefs aria-hidden='true'%3e %3cpath stroke-width='1' id='E1-MJMATHI-79' d='M21 287Q21 301 36 335T84 406T158 442Q199 442 224 419T250 355Q248 336 247 334Q247 331 231 288T198 191T182 105Q182 62 196 45T238 27Q261 27 281 38T312 61T339 94Q339 95 344 114T358 173T377 247Q415 397 419 404Q432 431 462 431Q475 431 483 424T494 412T496 403Q496 390 447 193T391 -23Q363 -106 294 -155T156 -205Q111 -205 77 -183T43 -117Q43 -95 50 -80T69 -58T89 -48T106 -45Q150 -45 150 -87Q150 -107 138 -122T115 -142T102 -147L99 -148Q101 -153 118 -160T152 -167H160Q177 -167 186 -165Q219 -156 247 -127T290 -65T313 -9T321 21L315 17Q309 13 296 6T270 -6Q250 -11 231 -11Q185 -11 150 11T104 82Q103 89 103 113Q103 170 138 262T173 379Q173 380 173 381Q173 390 173 393T169 400T158 404H154Q131 404 112 385T82 344T65 302T57 280Q55 278 41 278H27Q21 284 21 287Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-28' d='M94 250Q94 319 104 381T127 488T164 576T202 643T244 695T277 729T302 750H315H319Q333 750 333 741Q333 738 316 720T275 667T226 581T184 443T167 250T184 58T225 -81T274 -167T316 -220T333 -241Q333 -250 318 -250H315H302L274 -226Q180 -141 137 -14T94 250Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMATHI-6D' d='M21 287Q22 293 24 303T36 341T56 388T88 425T132 442T175 435T205 417T221 395T229 376L231 369Q231 367 232 367L243 378Q303 442 384 442Q401 442 415 440T441 433T460 423T475 411T485 398T493 385T497 373T500 364T502 357L510 367Q573 442 659 442Q713 442 746 415T780 336Q780 285 742 178T704 50Q705 36 709 31T724 26Q752 26 776 56T815 138Q818 149 821 151T837 153Q857 153 857 145Q857 144 853 130Q845 101 831 73T785 17T716 -10Q669 -10 648 17T627 73Q627 92 663 193T700 345Q700 404 656 404H651Q565 404 506 303L499 291L466 157Q433 26 428 16Q415 -11 385 -11Q372 -11 364 -4T353 8T350 18Q350 29 384 161L420 307Q423 322 423 345Q423 404 379 404H374Q288 404 229 303L222 291L189 157Q156 26 151 16Q138 -11 108 -11Q95 -11 87 -5T76 7T74 17Q74 30 112 181Q151 335 151 342Q154 357 154 369Q154 405 129 405Q107 405 92 377T69 316T57 280Q55 278 41 278H27Q21 284 21 287Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-29' d='M60 749L64 750Q69 750 74 750H86L114 726Q208 641 251 514T294 250Q294 182 284 119T261 12T224 -76T186 -143T145 -194T113 -227T90 -246Q87 -249 86 -250H74Q66 -250 63 -250T58 -247T55 -238Q56 -237 66 -225Q221 -64 221 250T66 725Q56 737 55 738Q55 746 60 749Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-3D' d='M56 347Q56 360 70 367H707Q722 359 722 347Q722 336 708 328L390 327H72Q56 332 56 347ZM56 153Q56 168 72 173H708Q722 163 722 153Q722 140 707 133H70Q56 140 56 153Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMATHI-62' d='M73 647Q73 657 77 670T89 683Q90 683 161 688T234 694Q246 694 246 685T212 542Q204 508 195 472T180 418L176 399Q176 396 182 402Q231 442 283 442Q345 442 383 396T422 280Q422 169 343 79T173 -11Q123 -11 82 27T40 150V159Q40 180 48 217T97 414Q147 611 147 623T109 637Q104 637 101 637H96Q86 637 83 637T76 640T73 647ZM336 325V331Q336 405 275 405Q258 405 240 397T207 376T181 352T163 330L157 322L136 236Q114 150 114 114Q114 66 138 42Q154 26 178 26Q211 26 245 58Q270 81 285 114T318 219Q336 291 336 325Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-30' d='M96 585Q152 666 249 666Q297 666 345 640T423 548Q460 465 460 320Q460 165 417 83Q397 41 362 16T301 -15T250 -22Q224 -22 198 -16T137 16T82 83Q39 165 39 320Q39 494 96 585ZM321 597Q291 629 250 629Q208 629 178 597Q153 571 145 525T137 333Q137 175 145 125T181 46Q209 16 250 16Q290 16 318 46Q347 76 354 130T362 333Q362 478 354 524T321 597Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-2B' d='M56 237T56 250T70 270H369V420L370 570Q380 583 389 583Q402 583 409 568V270H707Q722 262 722 250T707 230H409V-68Q401 -82 391 -82H389H387Q375 -82 369 -68V230H70Q56 237 56 250Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-31' d='M213 578L200 573Q186 568 160 563T102 556H83V602H102Q149 604 189 617T245 641T273 663Q275 666 285 666Q294 666 302 660V361L303 61Q310 54 315 52T339 48T401 46H427V0H416Q395 3 257 3Q121 3 100 0H88V46H114Q136 46 152 46T177 47T193 50T201 52T207 57T213 61V578Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-2212' d='M84 237T84 250T98 270H679Q694 262 694 250T679 230H98Q84 237 84 250Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMATHI-65' d='M39 168Q39 225 58 272T107 350T174 402T244 433T307 442H310Q355 442 388 420T421 355Q421 265 310 237Q261 224 176 223Q139 223 138 221Q138 219 132 186T125 128Q125 81 146 54T209 26T302 45T394 111Q403 121 406 121Q410 121 419 112T429 98T420 82T390 55T344 24T281 -1T205 -11Q126 -11 83 42T39 168ZM373 353Q367 405 305 405Q272 405 244 391T199 357T170 316T154 280T149 261Q149 260 169 260Q282 260 327 284T373 353Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-2F' d='M423 750Q432 750 438 744T444 730Q444 725 271 248T92 -240Q85 -250 75 -250Q68 -250 62 -245T56 -231Q56 -221 230 257T407 740Q411 750 423 750Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMATHI-3BB' d='M166 673Q166 685 183 694H202Q292 691 316 644Q322 629 373 486T474 207T524 67Q531 47 537 34T546 15T551 6T555 2T556 -2T550 -11H482Q457 3 450 18T399 152L354 277L340 262Q327 246 293 207T236 141Q211 112 174 69Q123 9 111 -1T83 -12Q47 -12 47 20Q47 37 61 52T199 187Q229 216 266 252T321 306L338 322Q338 323 288 462T234 612Q214 657 183 657Q166 657 166 673Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-32' d='M109 429Q82 429 66 447T50 491Q50 562 103 614T235 666Q326 666 387 610T449 465Q449 422 429 383T381 315T301 241Q265 210 201 149L142 93L218 92Q375 92 385 97Q392 99 409 186V189H449V186Q448 183 436 95T421 3V0H50V19V31Q50 38 56 46T86 81Q115 113 136 137Q145 147 170 174T204 211T233 244T261 278T284 308T305 340T320 369T333 401T340 431T343 464Q343 527 309 573T212 619Q179 619 154 602T119 569T109 550Q109 549 114 549Q132 549 151 535T170 489Q170 464 154 447T109 429Z'%3e%3c/path%3e %3cpath stroke-width='1' id='E1-MJMAIN-33' d='M127 463Q100 463 85 480T69 524Q69 579 117 622T233 665Q268 665 277 664Q351 652 390 611T430 522Q430 470 396 421T302 350L299 348Q299 347 308 345T337 336T375 315Q457 262 457 175Q457 96 395 37T238 -22Q158 -22 100 21T42 130Q42 158 60 175T105 193Q133 193 151 175T169 130Q169 119 166 110T159 94T148 82T136 74T126 70T118 67L114 66Q165 21 238 21Q293 21 321 74Q338 107 338 175V195Q338 290 274 322Q259 328 213 329L171 330L168 332Q166 335 166 348Q166 366 174 366Q202 366 232 371Q266 376 294 413T322 525V533Q322 590 287 612Q265 626 240 626Q208 626 181 615T143 592T132 580H135Q138 579 143 578T153 573T165 566T175 555T183 540T186 520Q186 498 172 481T127 463Z'%3e%3c/path%3e %3c/defs%3e %3cg stroke='currentColor' fill='currentColor' stroke-width='0' transform='matrix(1 0 0 -1 0 0)' aria-hidden='true'%3e %3cg transform='translate(167%2c0)'%3e %3cg transform='translate(-11%2c0)'%3e %3cg transform='translate(0%2c-22)'%3e %3cuse xlink:href='%23E1-MJMATHI-79' x='0' y='0'%3e%3c/use%3e %3cuse xlink:href='%23E1-MJMAIN-28' x='497' y='0'%3e%3c/use%3e %3cuse xlink:href='%23E1-MJMATHI-6D' x='887' y='0'%3e%3c/use%3e %3cuse xlink:href='%23E1-MJMAIN-29' x='1765' y='0'%3e%3c/use%3e %3cuse xlink:href='%23E1-MJMAIN-3D' x='2432' y='0'%3e%3c/use%3e %3cg transform='translate(3489%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-62' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-30' x='607' y='-213'%3e%3c/use%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-2B' x='4594' y='0'%3e%3c/use%3e %3cg transform='translate(5595%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-62' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='607' y='-213'%3e%3c/use%3e %3c/g%3e %3cg transform='translate(6478%2c0)'%3e %3cg transform='translate(120%2c0)'%3e %3crect stroke='none' width='3343' height='60' x='0' y='220'%3e%3c/rect%3e %3cg transform='translate(60%2c503)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2212' x='500' y='0'%3e%3c/use%3e %3cg transform='translate(904%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-65' x='0' y='0'%3e%3c/use%3e %3cg transform='translate(329%2c261)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-2212' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-6D' x='778' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-2F' x='1657' y='0'%3e%3c/use%3e %3cg transform='translate(1238%2c0)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-31' x='583' y='-323'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cg transform='translate(798%2c-476)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-6D' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2F' x='878' y='0'%3e%3c/use%3e %3cg transform='translate(975%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-31' x='718' y='-243'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-2B' x='10284' y='0'%3e%3c/use%3e %3cg transform='translate(11284%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-62' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-32' x='607' y='-213'%3e%3c/use%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-28' x='12168' y='0'%3e%3c/use%3e %3cg transform='translate(12557%2c0)'%3e %3cg transform='translate(120%2c0)'%3e %3crect stroke='none' width='2896' height='60' x='0' y='220'%3e%3c/rect%3e %3cg transform='translate(60%2c503)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2212' x='500' y='0'%3e%3c/use%3e %3cg transform='translate(904%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-65' x='0' y='0'%3e%3c/use%3e %3cg transform='translate(329%2c261)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-6D' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-2F' x='878' y='0'%3e%3c/use%3e %3cg transform='translate(791%2c0)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-31' x='583' y='-323'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cg transform='translate(575%2c-476)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-6D' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2F' x='878' y='0'%3e%3c/use%3e %3cg transform='translate(975%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-31' x='718' y='-243'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-2212' x='15916' y='0'%3e%3c/use%3e %3cg transform='translate(16917%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-65' x='0' y='0'%3e%3c/use%3e %3cg transform='translate(466%2c362)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2212' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-6D' x='778' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2F' x='1657' y='0'%3e%3c/use%3e %3cg transform='translate(1525%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-31' x='718' y='-243'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-29' x='19779' y='0'%3e%3c/use%3e %3cuse xlink:href='%23E1-MJMAIN-2B' x='20391' y='0'%3e%3c/use%3e %3cg transform='translate(21392%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-62' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-33' x='607' y='-213'%3e%3c/use%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-28' x='22275' y='0'%3e%3c/use%3e %3cg transform='translate(22665%2c0)'%3e %3cg transform='translate(120%2c0)'%3e %3crect stroke='none' width='2896' height='60' x='0' y='220'%3e%3c/rect%3e %3cg transform='translate(60%2c503)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2212' x='500' y='0'%3e%3c/use%3e %3cg transform='translate(904%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-65' x='0' y='0'%3e%3c/use%3e %3cg transform='translate(329%2c261)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-6D' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-2F' x='878' y='0'%3e%3c/use%3e %3cg transform='translate(791%2c0)'%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-32' x='583' y='-323'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cg transform='translate(575%2c-476)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-6D' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2F' x='878' y='0'%3e%3c/use%3e %3cg transform='translate(975%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-32' x='718' y='-243'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-2212' x='26023' y='0'%3e%3c/use%3e %3cg transform='translate(27024%2c0)'%3e %3cuse xlink:href='%23E1-MJMATHI-65' x='0' y='0'%3e%3c/use%3e %3cg transform='translate(466%2c362)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2212' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-6D' x='778' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-2F' x='1657' y='0'%3e%3c/use%3e %3cg transform='translate(1525%2c0)'%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.574)' xlink:href='%23E1-MJMAIN-32' x='718' y='-243'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3cuse xlink:href='%23E1-MJMAIN-29' x='29887' y='0'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/svg%3e)

where ' aria-hidden='true'%3e %3cuse xlink:href='%23E1-STIXWEBNORMALI-1D45A' x='156' y='-50'%3e%3c/use%3e %3c/g%3e %3c/svg%3e) is maturity,

is maturity, ' aria-hidden='true'%3e %3cg transform='translate(167%2c0)'%3e %3cg transform='translate(-11%2c0)'%3e %3cg transform='translate(0%2c-50)'%3e %3cuse xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='825' y='-213'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/svg%3e) and

and' aria-hidden='true'%3e %3cg transform='translate(167%2c0)'%3e %3cg transform='translate(-11%2c0)'%3e %3cg transform='translate(0%2c-50)'%3e %3cuse xlink:href='%23E1-MJMATHI-3BB' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-32' x='825' y='-213'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/svg%3e) control the curve shape, and

control the curve shape, and' aria-hidden='true'%3e %3cg transform='translate(167%2c0)'%3e %3cg transform='translate(-11%2c0)'%3e %3cg transform='translate(0%2c-50)'%3e %3cuse xlink:href='%23E1-MJMATHI-62' x='0' y='0'%3e%3c/use%3e %3cuse transform='scale(0.707)' xlink:href='%23E1-MJMAIN-31' x='607' y='-213'%3e%3c/use%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/g%3e %3c/svg%3e) is the long-term rate.

is the long-term rate.

Calibration

The short-term rates are first linear-interpolated to have 1, 3, 6 and 12 months rates. These interpolated rates are used in the calibration. For the long-term extrapolation, the following constraints are added:

Add a punishment in the target function to avoid non-monotone extrapolation.

The yield at the maximum horizon (100 years) is required to fall within 1% of market yields for the longest available horizon (typically, 15 to 30 years).

Linear interpolation is used between the longest horizon (100 years) from the longest market data available (15-30 years) if extrapolated rates are not monotone.

In periods of data instability (e.g. 2008), the two parametersandcan also be calibrated by hand to prevent unstable model calibrations.

Summary diagram

Example yield curves

1999 to 2020

US yield curves (click to enlarge animation)

Germany yield curves (click to enlarge animation)

France yield curves (click to enlarge animation)