Why do contributed indices tend to be biased?

Answer

Our Market indices are calculated indices built on the basis of a representative Index Universe.

Contributed indices like the ones published by Preqin or MSCI only use data contributed by an ad hoc group of investors. They do not attempt to determine what the underlying investable population might look like and only rely on what data can be contributed at each point in time.

This poses several problems:

Selection biases (also see here)

There is no clear or formal definition of the universe. The data used is whatever the contributing asset managers decide to contribute.

The data is arbitrarily skewed towards certain sectors or business models as per the contributors' portfolios.

The data is not consistent in time, different constituents find their way in and out of the universe without any logic or control.

The data may include the same asset multiple times (contributed by several managers).

The data is typically reported in USD, preventing any understanding of the roles of foreign exchange rates on changes in asset value.

Survivorship biases (also see here)

As reporting is voluntary, contributed data may not necessarily include all the assets of each investor. Non-performing assets may be omitted.

Non-performing or distressed assets tend to be disposed of in fund and investor portfolios, hence only the 'better investments' will tend to be represented in such datasets.

Time lag (backward-looking bias)

Private investment data is usually reported on a quarterly basis but it takes time for this information to be continued to data providers. The resulting time lag is between 3 and 6 quarters.

Things to Consider

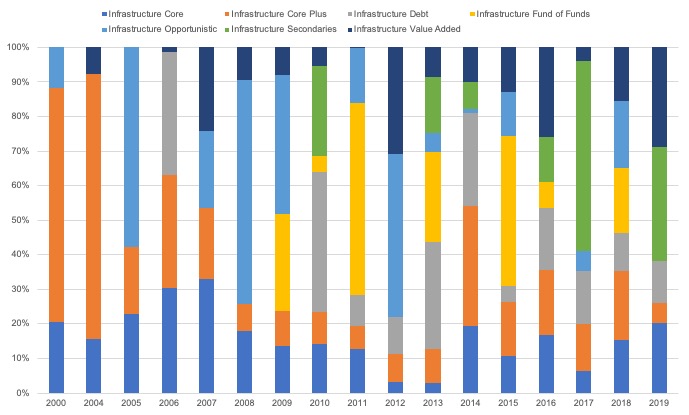

An example of the biases introduced in contributed indices can be seen in the range of infrastructure funds data available in the Preqin universe of infrastructure investments. The figure below suggest that the weight of each type of strategy changes each year as different contributors provide data.

Amongst the issues present in this type of data is the lack of clear definition of the strategies used to categorise the reported data. Depending on how funds self-defined their strategy in any given year ('infrastructure opportunistic' and 'secondaries'?) the breakdown can be difficult to interpret.

An objective, industry-backed taxonomy like TICCS® is designed to address these issues and built a representative sample of the investable universe.

Reported Infrastructure Fund Performance Data by Strategy, weighted by AUM. Source: Preqin, 2020