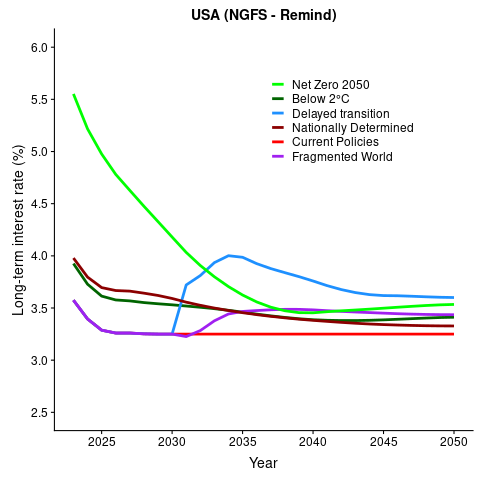

c) interest rates

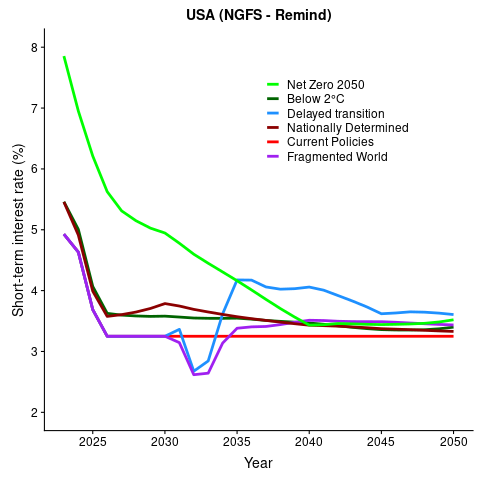

Being related to risk premia and discount rates, interest rates play a significant role in our asset pricing models. The figures below show the projections of long- and short-term interest rates in all scenarios. In NGFS, both short- and long-term interest rates start at a very high level in the Net Zero 2050 scenario. Specifically, the short-term rate before 2025 reflects the economy of the United States in the 1980s. Given the recent global macroeconomic developments, such levels are unlikely.

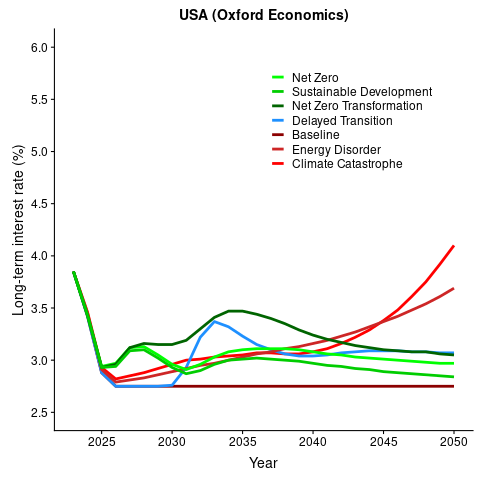

Projections of long-term interest rates in the United States for all NGFS (left) and Oxford Economics (right) scenarios.

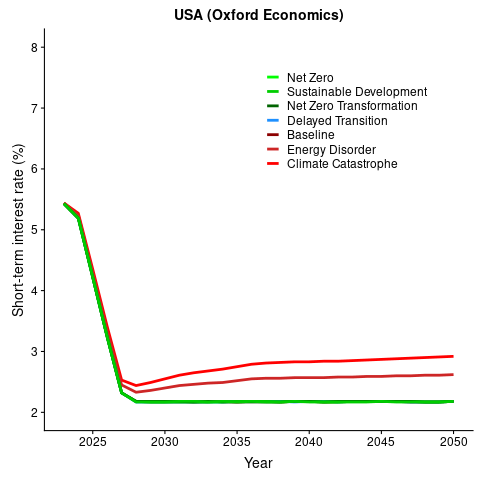

Projections of short-term interest rates in the United States for all NGFS (left) and Oxford Economics (right) scenarios.

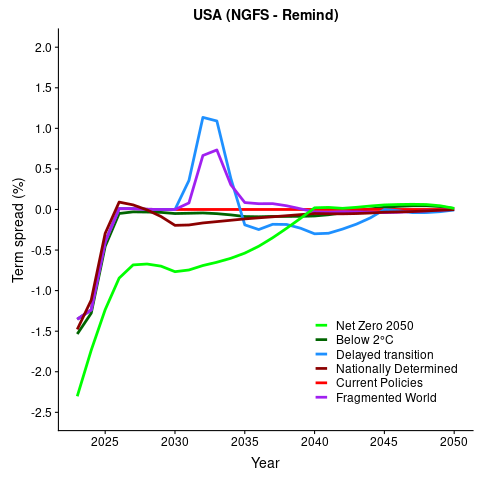

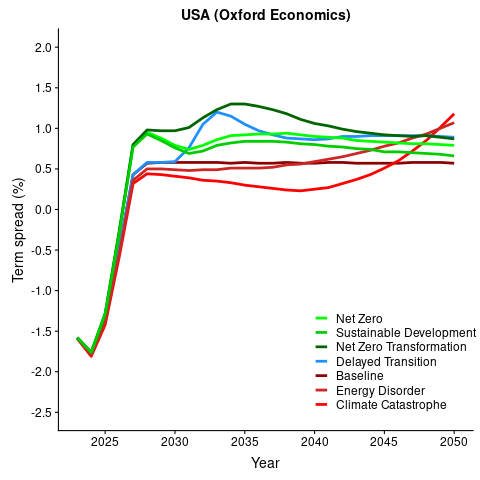

The figure below represents the projections of the term spread – the difference between the long- and short-term interest rates – for all NGFS and Oxford Economics scenarios. A low or negative term spread is generally viewed as a sign of a macroeconomic anomaly. According to the NGFS scenarios, the term spread is more likely to become negative compared to the Oxford Economics scenarios that present a consistently positive term spread from around 2028 onwards.

Term spread projections in the United States for all NGFS (left) and Oxford Economics (right) scenarios.